For much of the past decade, investors looking to capitalize on the battery revolution have focused on lithium. More recently, graphite, nickel and rare earth elements have emerged as critical components of the global race to electrify transportation and build energy storage infrastructure.

Yet another material is quietly becoming one of the most strategically important inputs in the battery supply chain: high-purity phosphate.

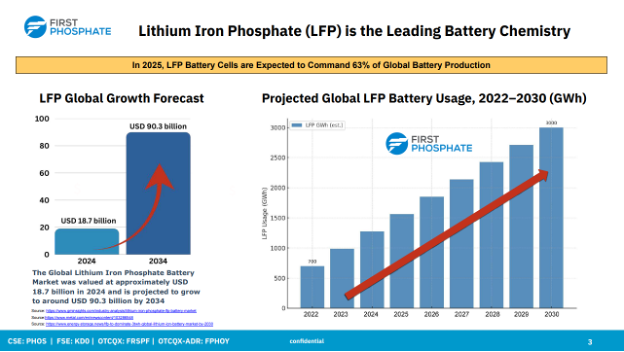

The growing importance of high-purity phosphate is closely tied to the rapid adoption of lithium iron phosphate (LFP) batteries, a chemistry that has evolved from a lower-cost alternative to nickel-rich batteries into one of the dominant technologies powering electric vehicles, grid-scale energy storage systems and next-generation infrastructure. As manufacturers increasingly prioritize safety, longevity and cost efficiency, LFP batteries have gained market share across multiple end markets, particularly in stationary energy storage applications.

(SOURCE: First Phosphate)

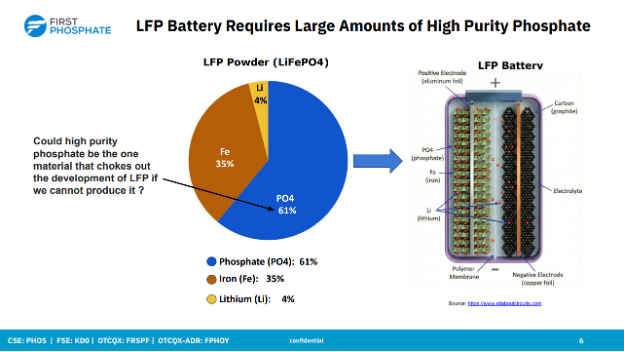

What makes this trend particularly significant is the amount of high-purity phosphate required. Unlike lithium, which often captures headlines and investor attention, high-purity phosphate represents roughly 60% of the cathode material in an LFP battery by weight, making it one of the largest material inputs in the chemistry. As North America works to establish an independent battery manufacturing ecosystem, secure access to high-purity battery-grade phosphate is emerging as a critical challenge.

(SOURCE: First Phosphate)

The result is a growing realization among policymakers, manufacturers and investors that high-purity phosphate may represent one of the most overlooked bottlenecks in the Western battery supply chain.

A Perfect Storm Is Forming in Global Phosphate Markets

The strategic importance of high-purity phosphate is becoming more apparent at a time when global supply chains are facing unprecedented pressure.

Over the past several months, sulfur prices—a key input used in traditional phosphate processing—have surged dramatically amid geopolitical disruptions and tightening supply conditions. Industry participants have pointed to disruptions affecting trade flows through the Strait of Hormuz, a critical chokepoint for global sulfur shipments, creating cost pressures across the phosphate industry. According to industry reports, sulfur prices have climbed above $1,200 per tonne, raising concerns about profitability and supply security for conventional phosphate producers.

The impact is already being felt among established industry players. Mosaic, one of the world's largest phosphate producers, recently withdrew its 2026 phosphate production guidance as rising sulfur costs and supply uncertainty complicated operating forecasts. Meanwhile, Nutrien has reportedly begun evaluating strategic alternatives for portions of its phosphate business, highlighting the challenges facing traditional producers that remain heavily exposed to global commodity markets.

These developments reflect a broader shift underway within the sector. For years, phosphate was viewed primarily through the lens of fertilizer demand. Today, market participants are increasingly focused on supply resilience, geopolitical risk and the availability of battery-grade material.

As governments seek to secure domestic critical mineral supply chains and manufacturers attempt to reduce dependence on overseas suppliers, the discussion is moving beyond simple commodity pricing. The central question has become whether North America can establish a reliable source of high-purity battery-grade phosphate before demand accelerates further.

The Rise of LFP Creates a New Strategic Demand Driver

The urgency surrounding high-purity phosphate supply is being amplified by the continued expansion of the LFP battery market.

Once viewed primarily as a lower-cost battery chemistry for entry-level electric vehicles, LFP has evolved into a cornerstone technology for the global energy transition. Its combination of safety, durability and cost effectiveness has made it particularly attractive for stationary energy storage systems, where reliability and longevity often matter more than maximizing energy density.

That shift is creating a powerful new source of demand for high-purity battery-grade phosphate.

The growth of renewable energy installations and utility-scale battery projects has already established energy storage as one of the fastest-growing segments of the broader battery market. Increasingly, LFP batteries are becoming the preferred chemistry for these applications, helping drive demand for purified phosphoric acid (PPA), a critical precursor material used in LFP cathode production.

Now, another catalyst is emerging.

The rapid buildout of artificial intelligence infrastructure is creating new demand for large-scale backup power and energy storage systems capable of supporting increasingly power-hungry data centers. Industry executives and analysts have begun highlighting LFP batteries as a preferred solution for data center energy storage because of their safety profile, thermal stability and long operating life. As a result, high-purity phosphate is gaining exposure to a new investment theme that extends well beyond electric vehicles.

For investors, this represents a notable shift. The phosphate story is no longer solely tied to EV adoption or agricultural markets. Instead, it is becoming linked to three of the most powerful secular growth trends in the global economy: electrification, energy storage and artificial intelligence infrastructure.

Government Policy is Accelerating Domestic Sourcing

Market forces alone are not driving the growing focus on high-purity phosphate. Government policy is increasingly reinforcing the need for domestic battery material supply chains.

In both the United States and Canada, policymakers have spent the past several years attempting to reduce dependence on foreign sources of critical minerals.

One of the most significant developments has been the implementation of stricter Foreign Entity of Concern (FEOC) requirements tied to U.S. battery incentives. Manufacturers seeking to qualify for federal tax credits must demonstrate that critical components and materials are sourced from compliant supply chains with limited Chinese influence. As regulators begin conducting more rigorous compliance reviews, battery producers are facing growing pressure to secure alternative sources of key materials.

At the same time, federal support for domestic battery manufacturing remains substantial. Recent policy initiatives have preserved advanced manufacturing incentives for battery cells and electrode materials, encouraging companies to localize production across the supply chain. These incentives are helping drive investment into domestic mining, refining and battery material processing capacity throughout North America.

Major Capital is Starting to Validate the Theme

The growing strategic importance of high-purity phosphate is increasingly being reflected in corporate transactions and capital allocation decisions across the sector.

One of the clearest signals emerged in May when Avenir Minerals, backed by gold-mining giant Agnico Eagle, agreed to acquire Fox River Resources in a transaction valued at approximately C$94 million. The deal attracted attention not only because of its size, but because it represented one of the strongest endorsements yet of North American igneous phosphate assets and their potential role in the battery supply chain. For many investors, the transaction served as evidence that sophisticated industry participants are beginning to view phosphate through a critical-minerals lens rather than a traditional fertilizer lens.

Technical milestones elsewhere in the sector have further strengthened that narrative.

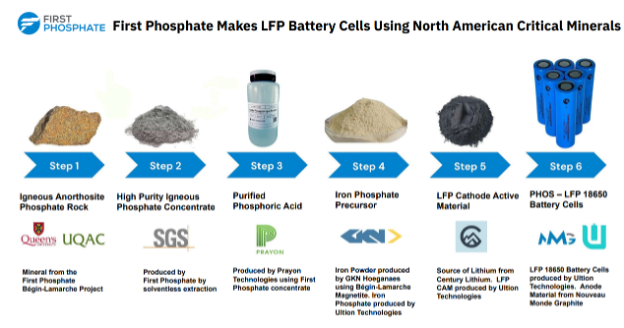

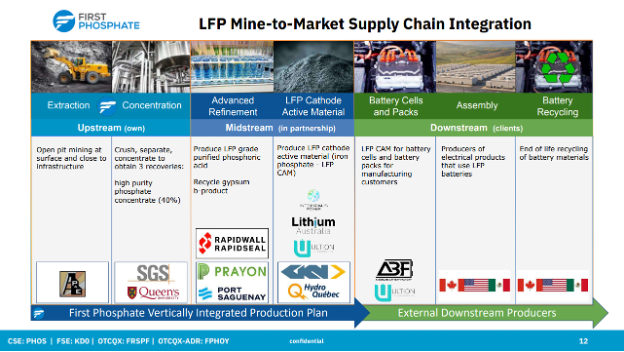

In Quebec, First Phosphate became the first to successfully demonstrate a North American mine-to-market pathway for LFP battery production, advancing material from high-purity phosphate-bearing igneous anorthosite ore through six stages of processing to finished LFP battery cells. The achievement highlights the potential for North American critical minerals to support domestic production of high-purity battery-grade phosphate materials and LFP batteries, reducing reliance on overseas supply chains. Globally, igneous phosphate is extremely rare, representing just 1% of the world’s phosphate.

(SOURCE: First Phosphate)

Meanwhile, industry participants are increasingly emphasizing supply security over commodity cycles. Investors who once focused primarily on short-term phosphate pricing are now paying closer attention to questions of jurisdiction, processing capability, geopolitical exposure and access to battery-grade feedstocks.

Taken together, these developments suggest that phosphate is undergoing a broader re-rating within the market. What was once viewed largely as an agricultural input is increasingly being recognized as a strategic material that sits at the intersection of electrification, energy storage, artificial intelligence infrastructure and industrial policy.

Why First Phosphate Stands Out

Having demonstrated a North American mine-to-market pathway for LFP battery production, First Phosphate (CSE: PHOS) (OTCQX: FRSPF) is advancing a strategy focused on supplying the high-purity phosphate and downstream materials required for the rapidly growing LFP battery market.

What distinguishes First Phosphate from many traditional phosphate producers is its singular focus on battery applications rather than fertilizer markets. While most global phosphate production ultimately serves agriculture, First Phosphate has built its strategy around supplying the purified phosphoric acid (PPA) and related materials required for LFP battery manufacturing.

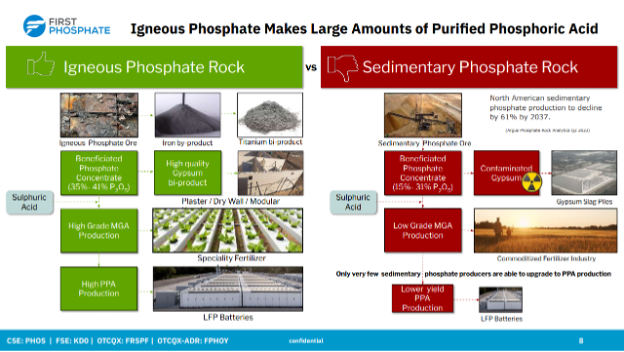

The company's asset base is centered in Quebec's Saguenay–Lac-Saint-Jean region, home to one of the few large-scale igneous phosphate districts in North America. Unlike sedimentary phosphate deposits that dominate global fertilizer production, igneous phosphate is generally valued for its purity characteristics and its suitability for conversion into battery-grade phosphoric acid.

(SOURCE: First Phosphate)

First Phosphate is pursuing a vertically integrated strategy that extends beyond mining, with plans that encompass phosphate extraction, purification, and downstream battery material production, allowing it to potentially participate in multiple stages of the value chain rather than remaining solely a raw-material supplier. This approach aligns with broader North American efforts to localize battery supply chains and reduce dependence on imported processing capacity.

(SOURCE: First Phosphate)

Recent developments have helped advance that strategy. The company received a C$16.7 million non-repayable contribution from the Government of Canada to support feasibility studies and process validation work, while also securing preliminary financing support from export credit agencies that could provide access to future project funding.

Several potential catalysts remain on the horizon. The company expects updated geological modeling and resource work following an extensive drilling campaign, alongside continued progress toward a feasibility study and potential commercial agreements. While execution risks remain typical of any development-stage mining project, First Phosphate appears increasingly aligned with several of the most important themes shaping the critical minerals sector: battery supply-chain localization, energy security and the buildout of North American manufacturing capacity.

The Next Phase of Battery Reshoring

Recent developments across the industry suggest that the market is beginning to recognize the strategic role high-purity phosphate plays in enabling LFP battery production. The combination of accelerating energy-storage deployment, AI-driven infrastructure investment, tightening sourcing requirements and growing geopolitical uncertainty is drawing renewed attention to a material that historically received little consideration outside fertilizer markets.

At the same time, a series of industry milestones—from major acquisitions and processing breakthroughs to government support for domestic supply chains—indicates that high-purity phosphate is increasingly being viewed as a critical mineral in its own right rather than merely a commodity input. The emerging narrative is less about fertilizer demand and more about industrial policy, energy security and the infrastructure required to support the next generation of economic growth.

Whether North America can develop sufficient high-purity battery-grade phosphate supply remains an open question. What appears increasingly clear, however, is that the importance of the material is rising. As manufacturers seek secure, compliant and geographically resilient sources of supply, companies capable of delivering high-purity battery-grade phosphate may find themselves occupying a strategically important position within the evolving battery ecosystem.

Disclosure

RedChip Companies, Inc. research reports, company profiles and other investor relations materials, publications or presentations, including web content, are based on data obtained from sources we believe to be reliable but are not guaranteed as to accuracy and are not purported to be complete. As such, the information should not be construed as advice designed to meet the particular investment needs of any investor. Any opinions expressed in RedChip reports, company profiles, or other investor relations materials and presentations are subject to change. RedChip Companies and its affiliates may buy and sell shares of securities or options of the issuers mentioned on this website at any time.

The information contained herein is not intended to be used as the basis for investment decisions and should not be construed as advice intended to meet the particular investment needs of any investor. The information contained herein is not a representation or warranty and is not an offer or solicitation of an offer to buy or sell any security. To the fullest extent of the law, RedChip Companies, Inc., our specialists, advisors, and partners will not be liable to any person or entity for the quality, accuracy, completeness, reliability or timeliness of the information provided, or for any direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information provided to any person or entity (including but not limited to lost profits, loss of opportunities, trading losses and damages that may result from any inaccuracy or incompleteness of this information).

Stock market investing is inherently risky. RedChip Companies is not responsible for any gains or losses that result from the opinions expressed on this website, in its research reports, company profiles or in other investor relations materials or presentations that it publishes electronically or in print.

We strongly encourage all investors to conduct their own research before making any investment decision. For more information on stock market investing, visit the Securities and Exchange Commission ("SEC") at www.sec.gov. and/or the Ontario Securities Commission (“OSC”) at www.osc.gov.on.ca.

First Phosphate (FRSPF) is a client of RedChip Companies. FRSPF agreed to pay RedChip Companies, Inc. a $10,000 monthly cash fee, beginning in December 2025, for six month of investor awareness services. A new agreement under the same terms extended services through December 31, 2026. FRSPF also agreed to pay RedChip a $150,000 fee for a two-week national TV ad campaign aired weekdays in January 2026. RedChip’s president acquired 75,000 shares of FRSPF in May 2026; these shares may be sold at any time, and you may be buying as they are sold.

Investor awareness services and programs are designed to help small-cap companies communicate their investment characteristics. RedChip investor awareness services include the preparation of a research profile(s), multimedia marketing, and other awareness services.