Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) is a small-cap healthcare software company operating in a critical but under-digitized part of the system—benefits administration for unions, third-party administrators (TPAs), and self-insured employers. Its platform is already embedded in client operations, generating 90% recurring revenue and 95% client retention, with a growing base of signed contracts and a clear path to scale to $100 million in signed contracts by 2028. With enterprise validation in place, a defined pipeline, and exposure to a $4-$6 billion market, the company is now shifting from foundation-building to growth—while still trading at a valuation that does not reflect that transition.

| Recent Price | $0.345 |

| Market Cap | $9.35M |

| 52-Week Range | $0.35265 - $0.7214 |

| Shares Outstanding | 28.99M |

| Volume | 20,000 |

(Source: Stock Analysis)

The Modernization Gap in Healthcare Administration

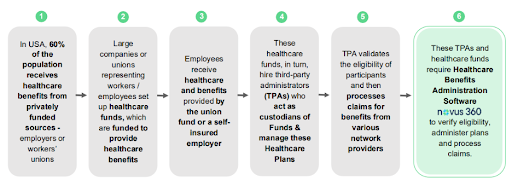

More than half of Americans receive healthcare through union-sponsored plans and self-insured employers, a system that operates largely outside traditional insurance models. Behind the scenes, these plans rely on a network of third-party administrators (TPAs) and internal systems to manage eligibility, process claims, ensure compliance, and communicate with members.

(Source: Comprehensive Healthcare Systems)

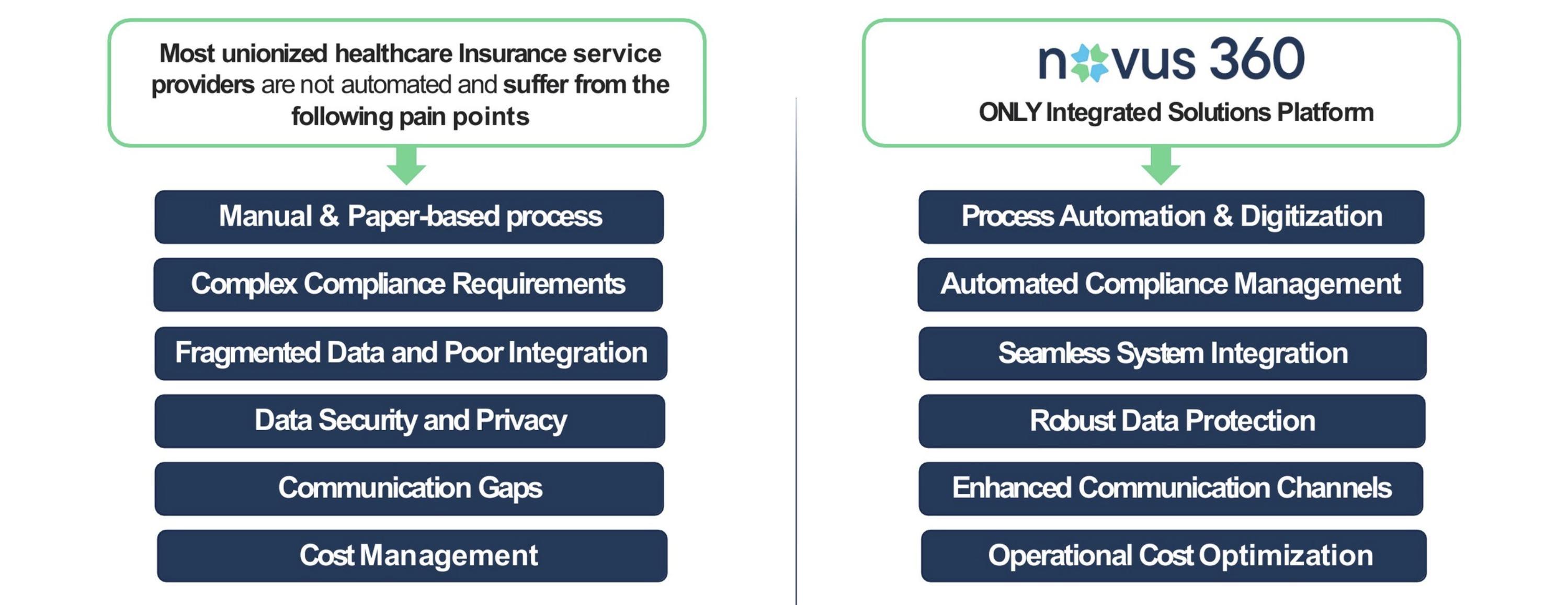

Much of this infrastructure still runs on fragmented, manual, and often outdated systems, where data sits in silos and critical processes depend on human intervention. This is not a peripheral issue—it is the operational backbone of healthcare delivery for more than 100 million people, and recent regulations are compounding the problem. The No Surprises Act, for example, requires health plans to provide accurate cost estimates, improve pricing transparency, and deliver clearer member communications—capabilities that legacy systems were never designed to support.

For investors, the opportunity is simple: the administrative complexity of modern healthcare has outgrown the systems built to manage it.

What Comprehensive Healthcare Systems Actually Does

Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) sits directly in the middle of this broken infrastructure layer with a product designed to replace it. Its core platform, Novus 360, is a fully integrated software platform that manages the entire lifecycle of healthcare and retirement benefits administration—built specifically for union plans, TPAs, and self-insured employers.

(Source: Comprehensive Healthcare Systems)

Rather than relying on a patchwork of systems, Novus 360 brings together eligibility management, claims processing, compliance tracking, and member engagement into a single environment, streamlining workflows that are typically fragmented across multiple vendors and manual processes.

Operating at the center of claims, eligibility, and compliance, the platform becomes embedded quickly and difficult to replace.

That shows up clearly in the numbers. Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) reports client retention above 95%, the kind of durability you typically see when software becomes part of the underlying operation, not just a vendor relationship.

It’s also already operating at meaningful scale, supporting more than one million members annually and processing over $1.8 billion in claims.

Revenue is tied directly to that usage. The company generates the majority of its revenue on a per-member-per-month (PMPM) basis, resulting in recurring revenue above 90%.

From Restructuring to Scalable Growth

What makes the story highly compelling today is not just the product—it’s the transition underway inside the business.

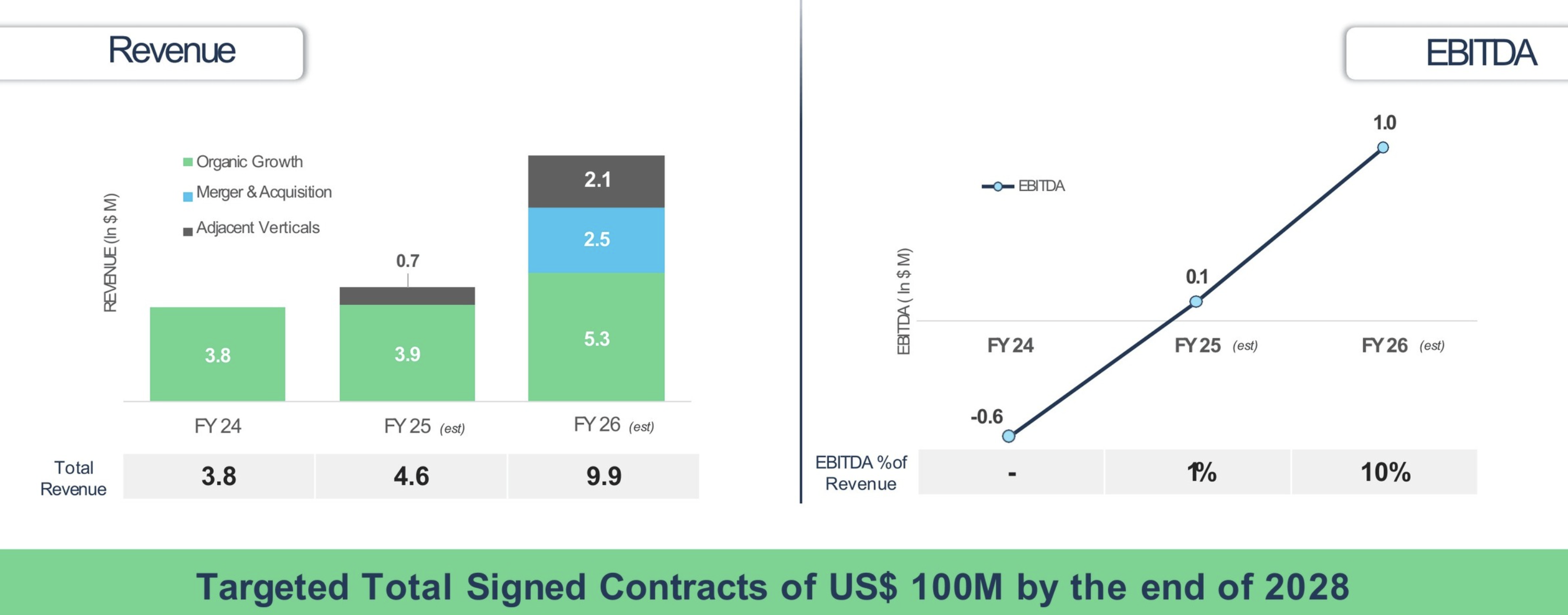

Over the past several years, Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) has repositioned the business around its core software platform, sharpening its strategic focus and aligning operations for scale. That groundwork is now reflected in a growing base of contracted revenue, with approximately C$35 million (US$25 million) in signed contracts across more than 20 clients, providing clear revenue visibility as the company moves into its next phase of growth.

With the platform established and a proven ability to scale, the focus shifts to execution—converting pipeline, onboarding new clients, and expanding within existing relationships. Management is targeting approximately $10 million in revenue in 2026, representing a meaningful step-up from trailing 12-month revenue of $4.2 million as of September 30, 2025.

Enterprise Validation: Proof at Scale

The clearest signal that this transition is gaining traction came in December 2025, when Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) signed a five-year, multi-million-dollar agreement with Amalgamated Life Insurance Company, one of the more established players in the Taft-Hartley union benefits market.

At the time of signing, the agreement represented roughly a 25% uplift to Comprehensive Healthcare Systems’ (OTCQB: CMHSF | TSXV: CHS) existing annual revenue base, a meaningful step-change for a company of this size.

More importantly, it’s a clear validation point. Amalgamated is a scaled operator in the union and multi-employer market, and its selection of Novus 360 followed an extensive evaluation process, ultimately coming down to the platform’s ability to handle complex, integrated environments.

For investors, that’s the signal. Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) can compete for—and win—large, operationally demanding clients. The question now is how quickly it can do it again.

Accelerating Commercial Expansion in a Multi-Billion-Dollar Market

Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) is operating within the $4–6 billion U.S. benefits administration software market, executing a strategy that extends beyond its core Taft-Hartley union base into TPAs and self-insured employers—segments facing the same underlying complexity and increasing demand for integrated solutions.

Today, the company has approximately $25 million in signed contracts and an active pipeline of roughly $20 million. Historically, roughly 25%–30% of pipeline has converted into signed contracts. The company is targeting $100 million in total contracts by 2028.

(Source: Comprehensive Healthcare Systems)

With the recent addition of an industry veteran as VP of Sales, the focus is on expanding its pipeline and improving conversion across larger, more complex opportunities.

The Re-Rating Setup: A Clear Valuation Disconnect

Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) currently trades at approximately 1.5x projected 2026 revenue, a level typically reserved for businesses without visibility, scale, or recurring revenue.

In contrast, private-market healthcare SaaS peers commonly command multiples in the 7x to 10x range, particularly for platforms with recurring revenue and high retention.

Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) already has the foundation those higher multiples are typically applied to: a recurring revenue model with a growing base of contracted revenue, retention above 95%, and a proven platform operating at enterprise scale.

At current levels, the market is not reflecting that profile. As the company executes against its existing contracts, converts pipeline, and moves toward its 2026 revenue targets, the disconnect between valuation and fundamentals becomes increasingly likely to close.

Risks

As a microcap company, Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) carries the typical risks associated with its size, including limited trading liquidity and potential volatility. Execution remains key, particularly in converting pipeline into signed contracts and scaling revenue in line with targets. The company may also require additional capital to support growth, and longer enterprise sales cycles can impact the timing of revenue realization.

The Investment Case

Strip the story down to its core, and the setup is straightforward. Comprehensive Healthcare Systems (OTCQB: CMHSF | TSXV: CHS) operates in a large, complex, and under-digitized segment of the healthcare system where software is not optional—it is mission-critical.

The company already has a working product, embedded relationships, and a growing base of contracted recurring revenue. It has demonstrated the ability to operate at scale, win larger enterprise clients, and expand beyond its core market into adjacent segments facing the same structural challenges.

From here, the path forward is defined by execution: converting pipeline, expanding contracts, and scaling a recurring revenue model within a multi-billion-dollar market.

At the same time, the current valuation does not reflect that trajectory. For investors, that combination—proven platform, visible growth, and a significant valuation gap—is where the opportunity lies.

Disclosure

RedChip Companies, Inc. research reports, company profiles and other investor relations materials, publications or presentations, including web content, are based on data obtained from sources we believe to be reliable but are not guaranteed as to accuracy and are not purported to be complete. As such, the information should not be construed as advice designed to meet the particular investment needs of any investor. Any opinions expressed in RedChip reports, company profiles, or other investor relations materials and presentations are subject to change. RedChip Companies and its affiliates may buy and sell shares of securities or options of the issuers mentioned on this website at any time.

The information contained herein is not intended to be used as the basis for investment decisions and should not be construed as advice intended to meet the particular investment needs of any investor. The information contained herein is not a representation or warranty and is not an offer or solicitation of an offer to buy or sell any security. To the fullest extent of the law, RedChip Companies, Inc., our specialists, advisors, and partners will not be liable to any person or entity for the quality, accuracy, completeness, reliability or timeliness of the information provided, or for any direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information provided to any person or entity (including but not limited to lost profits, loss of opportunities, trading losses and damages that may result from any inaccuracy or incompleteness of this information).

Stock market investing is inherently risky. RedChip Companies is not responsible for any gains or losses that result from the opinions expressed on this website, in its research reports, company profiles or in other investor relations materials or presentations that it publishes electronically or in print.

We strongly encourage all investors to conduct their own research before making any investment decision. For more information on stock market investing, visit the Securities and Exchange Commission ("SEC") at www.sec.gov. and/or the Ontario Securities Commission (“OSC”) at www.osc.gov.on.ca.

Comprehensive Healthcare (CMHSF) is a client of RedChip Companies. CMHSF agreed to pay RedChip Companies, Inc. a $7,500 monthly cash fee, beginning in January 2026, and 150,000 stock options for six month of investor awareness services. RedChip intends to and will, if possible, exercise and sell any options earned as soon as they are eligible to sell, and you may be buying as RedChip is selling. CMHSF also agreed to pay RedChip a $60,000 fee for a two-week national TV ad campaign aired in April 2026.

Investor awareness services and programs are designed to help small-cap companies communicate their investment characteristics. RedChip investor awareness services include the preparation of a research profile(s), multimedia marketing, and other awareness services.