First Phosphate Corp. (OTCQX-ADR: FPHOY | OTCQX: FRSPF | CSE: PHOS) is a Quebec-based critical minerals developer building a vertically integrated supply chain for lithium iron phosphate (LFP) battery materials in North America. The company's flagship Bégin-Lamarche Property in the Saguenay–Lac-Saint-Jean region of Quebec is a rare, large-scale igneous phosphate deposit being advanced toward a full feasibility study. On January 7, 2026, Mark Reichman, Managing Director of Equity Research at Noble Capital Markets, maintained an Outperform rating and a price target of US$1.55 per share on First Phosphate Corp., representing implied upside of approximately 104% from the share price of $0.76. Since that report, First Phosphate Corp. has completed its drill program, secured C$16.7 million in non-repayable federal funding, and seen phosphate formally designated a Canadian critical mineral, all of which materially strengthen the path toward a feasibility study by late 2026.

| Recent Price | $1.07 |

| Market Cap | $185.32M |

| 52-Week Range | $0.18915 - $0.9085 |

| Shares Outstanding | 173.27M |

| Volume | 69,872 |

(Source: Stock Analysis)

What First Phosphate Corp. Actually Does

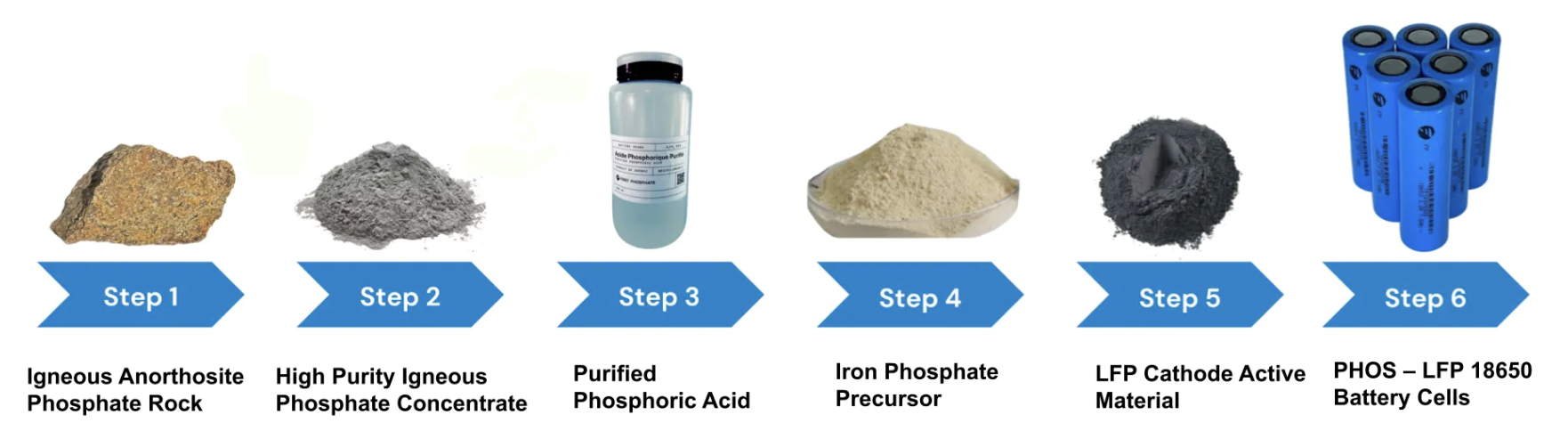

First Phosphate Corp. is singularly focused on supplying battery-grade phosphate for the LFP battery market, a strategy that sets it apart from conventional phosphate producers tied to the fertilizer industry. The company controls a rare igneous phosphate resource in Quebec, one of the few known deposits of this type globally, and is executing a mine-to-cathode strategy that spans mining, phosphate concentration, purified phosphoric acid (PPA) production, and iron-phosphate precursor materials.

(Source: First Phosphate Corp.)

PPA is the essential input for LFP cathode active material, which is the chemistry found inside batteries used in electric vehicles, grid-scale energy storage, data centers, and emerging technologies like robotics and AI infrastructure. First Phosphate Corp. intends to process concentrate from Bégin-Lamarche at a purified phosphoric acid plant at Port Saguenay and supply an iron-phosphate precursor facility at La Baie, forming a fully domestic, onshore supply chain designed for North American and European LFP markets. The company has already demonstrated that commercial-grade LFP 18650 battery cells can be produced using material sourced entirely from its Quebec property.

The Market Backdrop: LFP Batteries Are the Fastest-Growing Chemistry

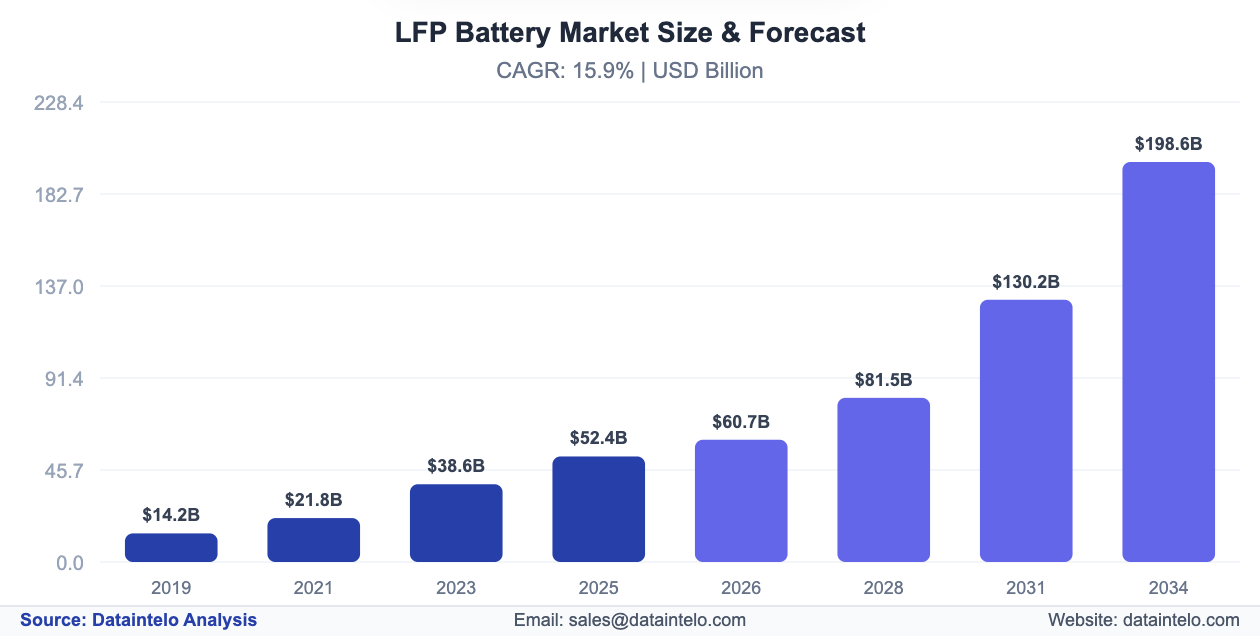

The structural case for First Phosphate Corp. begins with the rapid expansion of LFP battery demand. According to Data Intelo, the global LFP battery market was valued at approximately $52.4 billion in 2025 and is projected to grow to $198.6 billion by 2034, reflecting a compound annual growth rate of over 12%. Demand is being driven by electric vehicles, grid-scale energy storage, data center backup power, and industrial automation.

(Source: DataIntelo Analysis)

The International Energy Agency reported in early 2026 that batteries are becoming a cornerstone of the automotive sector, a critical source of flexibility for power systems, and an increasingly important source of back-up power for digital infrastructure, including data centers and artificial intelligence. That supply-chain concentration is the market gap First Phosphate Corp. is positioned to fill. Phosphate accounts for up to approximately 60% of LFP cathode chemistry by mass, making it the largest material input in the battery by volume. Western markets currently face a structural shortage of battery-grade PPA, and the supply of igneous phosphate capable of efficient conversion to that grade is exceptionally limited outside of China.

The Geological Edge: Why Igneous Phosphate Matters

Not all phosphate is equal in the context of battery materials. The majority of global phosphate resources are sedimentary in origin, a type that contains higher impurity levels and requires additional processing before it can meet battery-grade purity standards. Igneous phosphate, by contrast, delivers naturally higher P₂O₅ grades with fewer contaminants, making it a more efficient and cost-effective feedstock for PPA production.

(Source: First Phosphate Corp.)

Igneous deposits represent approximately 5% of global phosphate resources, which is what makes the Bégin-Lamarche property strategically significant. The updated resource at Bégin-Lamarche stands at 41.5 million tonnes indicated at 6.49% P₂O₅ and 214 million tonnes Inferred at 6.01% P₂O₅, supporting an estimated mine life of approximately 24 years. The property's preliminary economic assessment (PEA), completed in December 2024, outlines a 23-year open-pit operation producing approximately 900,000 tonnes per year of 40% phosphate concentrate with an NPV of approximately CAD $2.1 billion, an IRR of approximately 37%, and a roughly three-year payback period. Saleable magnetite and ilmenite by-products are expected to provide additional economic value.

(Source: First Phosphate Corp.)

The Saguenay–Lac-Saint-Jean region provides a compelling operating environment. The area is connected by established industrial infrastructure, sits approximately 70 kilometers from the Port of Saguenay and planned downstream processing sites, and is powered by Quebec's low-carbon hydroelectric grid, an important competitive and regulatory advantage for a project targeting carbon-conscious LFP markets in North America and Europe.

The EIFO Milestone: State-Backed Credit Enhancement at Scale

The catalyst behind Noble Capital Markets' target increase is the April 13, 2026 EIFO announcement. First Phosphate Corp. finalized a letter of intent from the Danish Export Credit Agency for up to €170 million in equipment and services purchases for Bégin-Lamarche. EIFO is Denmark's combined national promotional bank and official export credit agency, an independent public company guaranteed by the Danish state with an AAA credit rating. EIFO carries a portfolio of roughly €22 billion and has financed more than 30% of installed offshore wind capacity outside China, giving it deep experience underwriting large energy-transition projects.

The guarantee would be provided to one or more banks participating in project financing, with EIFO participation expected to be pro rata and pari passu alongside other senior lenders. For a development-stage company, this provides a highly credible layer of credit enhancement that can meaningfully lower borrowing costs on the senior debt portion of project financing. Issuance remains subject to EIFO's internal credit approval and customary project due diligence, and the letter is non-binding pending finalization of borrower and security arrangements.

Importantly, the EIFO letter does not stand alone. First Phosphate Corp. has been working since 2023 with the Export-Import Bank of the United States (EXIM) on a separate letter of interest for up to US$170 million to finance U.S. goods and services procurement. That letter was extended in October 2024 and is in the process of being extended again. State-backed credit support from both European and American institutions diversifies the procurement base and reduces reliance on any single export market.

Recent Strategic Developments: Major Milestones in 2026

First Phosphate Corp. has delivered a series of meaningful operational, financial, and policy developments over the past several months, culminating in the EIFO announcement that drove Noble Capital Markets' target increase.

(Source: First Phosphate Corp.)

On March 31, 2026, the company announced the completion of its infill drill program at Bégin-Lamarche. What began as a 30,000-metre program was expanded to 40,000 metres after drillers discovered two new phosphate intersections in the Northern and Southern Zones beyond the known resource boundary. The completed program confirmed extensive, continuous mineralization across the property and will feed directly into an updated geological model and the planned feasibility study targeted for late 2026.

Earlier in March 2026, First Phosphate Corp. finalized a C$16.7 million non-repayable contribution agreement with the Government of Canada through Natural Resources Canada's Global Partnerships Initiative. The funding is specifically designated for technical and engineering work needed to validate the ability to produce phosphate concentrate to LFP battery-grade quality standards. Because the contribution is non-repayable and non-dilutive, it represents a significant capital injection that supports the path to feasibility without adding debt or new shares outstanding.

In February 2026, Canada's federal budget added phosphate to the country's Critical Minerals list, making phosphate projects eligible for two 30% refundable tax credits: the Critical Mineral Exploration Tax Credit (CMETC) for exploration spending and the Clean Technology Manufacturing Investment Tax Credit (CTM) for investments in processing equipment and clean technology infrastructure. For First Phosphate Corp., these designations reduce both the cost of future exploration financing and the effective capital cost of the downstream processing facilities that form the core of its integrated strategy.

Capital Position and Financing Activity

As of early 2026, First Phosphate Corp. reported cash on hand of approximately C$27 million. This position reflects the completion of a C$9.6 million private placement closed in December 2025, subsequent warrant exercises in January 2026, and receipt of the US$530,000 offtake prepayment under the company's long-term phosphate concentrate supply agreement. The company has raised approximately C$49.7 million across ten management-led non-brokered private placements since its founding in June 2022. Importantly, the balance sheet carries no long-term debt, and Noble Capital Markets noted that liquidity is expected to be sufficient to fund planned activities through 2026 and into 2027.

The offtake prepayment is notable as a form of commercial validation. A downstream purchaser willing to commit capital upfront to secure future supply is a meaningful signal of real market demand, not just exploratory interest. The existence of a definitive offtaker also structured the NRCan contribution agreement, as the federal funding was specifically linked to technical work aligned with that offtaker's quality requirements.

The company was also added to the CSE25 Index, a benchmark of the 25 leading Canadian Securities Exchange companies by market capitalization and liquidity, effective December 2025. Index inclusion expands the company's visibility among institutional and retail investors at a time when it is transitioning from exploration to feasibility-level development.

How Noble Capital Markets Arrived at the US$1.65 Price Target

Noble Capital Markets analyst Mark Reichman derived his updated US$1.65 per share price target using a multi-stage discounted cash flow (DCF) model. A DCF model estimates the present value of all future cash flows a project is expected to generate, discounted back at a rate that reflects the risk of the investment. Reichman applied a 12.0% discount rate and assumed no terminal growth beyond the project's modeled life, consistent with a 23-year mine and processing plan.

The model incorporates full initial capital spending, sustaining capital requirements, operating cash flows across the ramp-up and steady-state phases, and closure costs at end of life. Using an exchange rate of US$0.73 per Canadian dollar, the US$1.65 target equates to approximately C$2.25 on the Canadian Securities Exchange. Noble's Outperform rating is defined as a potential return exceeding 15% above the current share price. The firm also assigns First Phosphate Corp. a fundamental assessment rating of 3.5 out of 5.0, which places the company in Noble's "Above Average" tier, citing a technically strong and policy-aligned leadership team, high-purity igneous phosphate assets with clear metallurgical advantages, and a supportive jurisdiction.

Risks

First Phosphate Corp. remains a pre-revenue development company and carries the risks common to early-stage mining projects. Advancing from feasibility to production will require significant capital for mine construction and the development of downstream PPA and iron-phosphate precursor facilities. Commodity price fluctuations, permitting timelines, and execution risk at each stage of the integrated value chain represent real uncertainties. The conditions attached to both the EIFO and EXIM letters of interest, which remain subject to formal credit approval and due diligence, also represent real uncertainties. The company will likely need to raise additional capital to fund construction, which could result in dilution to existing shareholders. Investors should consider these factors when evaluating the investment.

The Investment Argument

The convergence of events at First Phosphate Corp. over the past several months represents a meaningful de-risking of the development story. The drill program has been completed and expanded, with two new mineralization zones discovered. The resource underpins an estimated 24-year mine life. A C$16.7 million non-repayable federal contribution directly funds the technical work needed for feasibility. Phosphate's new critical mineral designation unlocks a pair of 30% tax credits. The balance sheet is debt-free with approximately C$27 million in cash. A downstream offtake partner has validated demand with a cash prepayment. And the project now has two separate, state-backed project-finance pathways in development, the EIFO guarantee of up to €170 million and the EXIM letter of interest for up to US$170 million, covering a combined amount well in excess of US$300 million.

Each of these developments individually would be notable for a junior mining company. Together, they represent a company that has methodically assembled the building blocks, geology, infrastructure, capital, regulatory recognition, international financing relationships, and commercial offtake that a feasibility study requires. With that study targeted for completion by late 2026 and Noble Capital Markets raising its price target to US$1.65 with an Outperform rating, the bull case at First Phosphate Corp. is grounded in a concrete, near-term development timeline rather than speculative upside alone.

Disclosure

RedChip Companies, Inc. research reports, company profiles and other investor relations materials, publications or presentations, including web content, are based on data obtained from sources we believe to be reliable but are not guaranteed as to accuracy and are not purported to be complete. As such, the information should not be construed as advice designed to meet the particular investment needs of any investor. Any opinions expressed in RedChip reports, company profiles, or other investor relations materials and presentations are subject to change. RedChip Companies and its affiliates may buy and sell shares of securities or options of the issuers mentioned on this website at any time.

The information contained herein is not intended to be used as the basis for investment decisions and should not be construed as advice intended to meet the particular investment needs of any investor. The information contained herein is not a representation or warranty and is not an offer or solicitation of an offer to buy or sell any security. To the fullest extent of the law, RedChip Companies, Inc., our specialists, advisors, and partners will not be liable to any person or entity for the quality, accuracy, completeness, reliability or timeliness of the information provided, or for any direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information provided to any person or entity (including but not limited to lost profits, loss of opportunities, trading losses and damages that may result from any inaccuracy or incompleteness of this information).

Stock market investing is inherently risky. RedChip Companies is not responsible for any gains or losses that result from the opinions expressed on this website, in its research reports, company profiles or in other investor relations materials or presentations that it publishes electronically or in print.

We strongly encourage all investors to conduct their own research before making any investment decision. For more information on stock market investing, visit the Securities and Exchange Commission ("SEC") at www.sec.gov. and/or the Ontario Securities Commission (“OSC”) at www.osc.gov.on.ca.

First Phosphate (PHOS) is a client of RedChip Companies. PHOS agreed to pay RedChip Companies, Inc. a $10,000 monthly cash fee, beginning in December 2025, for six month of investor awareness services. PHOS also agreed to pay RedChip a $150,000 fee for a two-week national TV ad campaign aired weekdays in January 2026.

Investor awareness services and programs are designed to help small-cap companies communicate their investment characteristics. RedChip investor awareness services include the preparation of a research profile(s), multimedia marketing, and other awareness services.